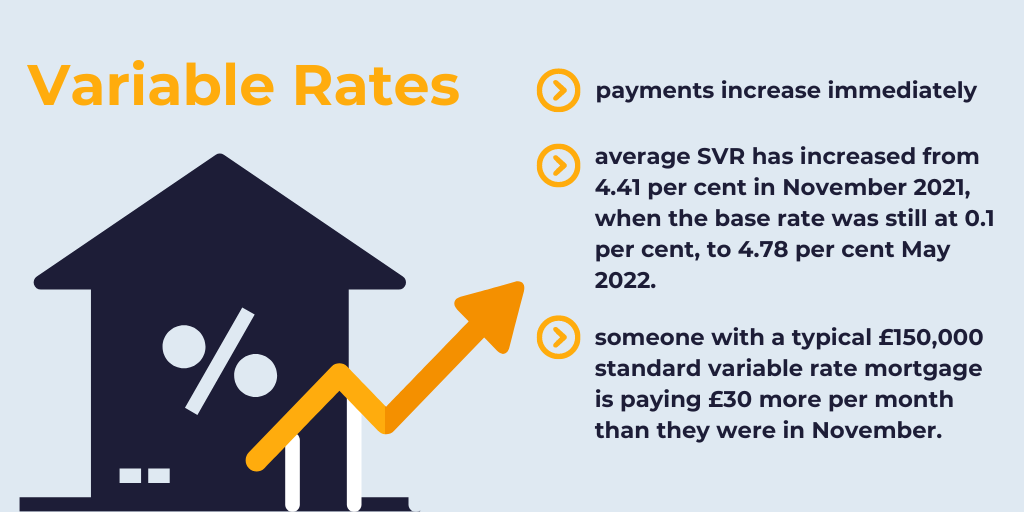

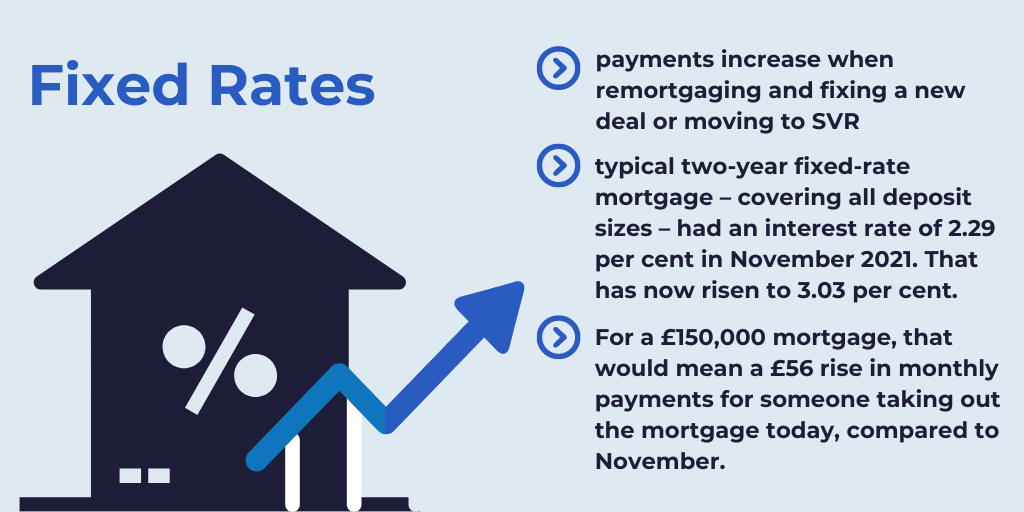

It might be worth speaking with your us sooner rather than later as we may be able to help you find a more suitable deal before you incur the higher costs associated with rising rates.

We face household accidents regularly, but that’s not to say they aren’t annoying to deal with when they happen. Many of us prefer to protect our assets and valuables just in case and while that won’t stop things getting broken, it does help during the aftermath, but what does Accidental Damage Insurance actually involve?

What is accidental damage?

Accidental damage is caused suddenly and unexpectedly by an outside force. It’s different from damage caused by wear and tear or a breakdown. You can add accidental damage cover to either your contents insurance or to your building’s insurance.

What’s likely to be covered:

If you are working, what would happen to your monthly income if you suddenly lost your ability to work?

Would you be able to manage without your monthly income?

If you could not pay your mortgage, how long before you lose your home? How would you pay the food bills and which of your home comforts would you lose first? Can you and your family cope with this financial loss?

Income Protection will pay you a monthly, tax-free income if you are signed off work by your GP, and the monthly payment starts after your chosen deferred period.

Case Study

Debbie was involved in a car accident which affected her ability to carry out her daily routine, including working as a full-time Chef.

As the main earner in her household, Debbie’s husband and 2 young children (aged 3 & 5) depend heavily on her monthly wage to pay the mortgage, bills and general household expenses.

Following her car accident, she contacted her insurance company and was offered emotional as well as physical support, including counselling and extra physio sessions. Debbie received 3 months sick pay, and the family had to use their savings for 3 months and the Income Protection policy started paying from then on.

When Debbie was advised to take out Income Protection, she was reluctant and waited over a year before she made her decision. She always felt that she would be making monthly payments for something she would never need.

After many discussions with her husband and Financial Adviser she eventually decided to take out the policy. If she had not made this decision, the family would have lost everything.

In this case, Debbie’s injuries were very severe after the car accident, and she could not carry out the manual duties required as a Chef. However, she did go back to a lower paid role and the Income Protection policy topped up the difference to the amount she had taken out, so the family had not lost anything financially.

It pays to be prepared especially if you don’t have significant savings or ‘rainy day’ funds. Don’t leave additional stress on your plate should the worst happen. Give us a call or drop us an email today to discuss your needs.

As we get older our needs change. We may find we have less stability and some of us may even see our overall health in decline. Does that mean you (or your loved ones) need to leave your home and move into residential care? Not necessarily. What if you could receive care at home and utilise equity tied up in your home to fund this?

By the time we’re looking at making home alterations or paying for visiting carers, we may also be at a position where we’ve amassed a significant sum of equity in our homes. And when it comes to paying for care at home, it’s no cheap option. If you earn under £23,250, you may qualify for help from your local authority, but if not, you could be looking at funding costs of up to £83,200 a year to remain in your home while receiving care.

Moneyhelper* suggest the following estimates for at home care:

- £15,000 a year, for 14 hours of care a week. Based on the UK Homecare Association’s estimate of what councils should pay, as a minimum it’s £20.69 an hour. If you’re self-funding, you might pay more.

- If you need full-time care during the day, costs could be more than double the above.

- If you need carers to move in around the clock and you have complex needs, it could cost about £83,200 a year. In those circumstances, residential care is usually more cost-effective. If you don’t have complex needs, fees should be less – about £41,000-£65,000 a year.

Even if you only require a small amount of support at home, or perhaps none at all, you can also look to releasing funds from your home to finance adapting the home for your developing needs. For example, adding a downstairs bathroom, adding a ramp to the entrance of your home, or even adding supportive handles in and around the home. Either way, the funds locked up in your home could help to secure these necessities as you require them.

If you or someone you know is in need of funding care at home, or home adaptations and equity release may be a solution for you, get in touch with our team today for a no obligation chat.

This is a lifetime mortgage. To understand the features and risks, ask for a personalised illustration. Check that this mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

The UK is amid a cost-of-living crisis. Prices are rising at rates we haven't seen since the 1970s – energy, broadband, water, council tax, food, fuel and more. So here are just a few handy tips for saving money where you can.

Ten top tips for saving money

- Heat the human, not the home: Luckily, we’re not in the middle of winter yet, so being cautious with our heating isn’t as imperative, but head of the winter months it’s important to start thinking about ways you can keep yourself warm (think extra layers and blankets!) to avoid switching the heating on where possible.

- Over 800,000 people could be eligible for Pension Credit

Pension credit is a tax-free, means-tested benefit aimed at retired people on low incomes – and it can be worth £1,000s a year. Plus, it's a gateway benefit that may make you eligible for council tax discounts, free TV licences for over-75s and more. - Fix it don’t throw it

When our big-ticket items face their demise, it can be a daunting prospect having to source the funds to replace them. Items such as laptops could be readily fixed at local ‘Repair Cafes’ saving you throwing hundreds at something that could be fixed yet.

- Check your connection

Millions of people are sat outside of contracts on their Broadband and mobile tariffs, meaning they’re incurring higher charges than needs be. Many contracts offer an initial cheaper period for the first 12 months, and hike the prices for the remainder. In this situation you need to ditch and find a new deal or in some cases (if you’re low income/in receipt of universal credit) you could qualify for what is known as a ‘social tariff’ on your broadband, where the good rates are fixed longer term. - The Pay challenge!

For those on minimum wage, you could be being underpaid as your pay may not cover all the time you’re classed as working, or they have to buy items to do their job. If so, you may be due £100s or £1,000s back. For those on salaried jobs, are you due an annual pay review? It doesn’t hurt to speak to your employer about a pay increase if you’re due one. - Reach out to your local authority

Local authorities are being granted funds to support those in their local communities, so it’s worth reaching out if you’re struggling. You needn’t be in receipt of benefits to qualify and your local authority may have ways to support you or be able to signpost other services for support. - Switch it up

Changing bank accounts can be an easy and free way to address your cashflow. Covid put stop to many offering this option, but they appear to be back on the climb again now. So, unless there’s a reason your bank has your unwavering loyalty, perhaps it’s time at looking to switch and earn up to £170 for free. - Are you eligible for benefits?

Many people think benefits are reserved exclusively for extremely low-income households, but if your family income is below £30,000 (or £50,000 in rare cases!) you could qualify for additional support in means tested benefits. Even qualifying for a small amount can open up doors to other cost saving options such as council tax reductions and reduced utility tariffs. - Pick up free groceries

Olio is a brilliant app for picking up groceries from stores that are nearing/just clearing their use by dates, as well as surplus stock. Not only could it save you some money, but it saves companies from throwing away usable food too. - Cover the childcare costs

Whether you have a wee tot or a big teen, childcare costs can be huge. Yet 100,000s of working parents are missing out on £1,000s of help with this expense. It's worth checking to see if you’re eligible for help. Explore schemes on offer for costs that can be covered, this can even include wrap around care.

If you know where to look there are hundreds of money saving tips for everyday expenses, that could help tackle the significant increases in everyday essentials.

Unless you’re been hiding from the latest news, you’ll likely have seen all the stories on cancelled flights and nightmares at the airports. But if your flight is cancelled, you're due an alternative or a full refund. If it's within 14 days of departure, you could be owed £100s in compensation on top.

If you're stuck at the airport or abroad, you can also claim back other costs

If you're stuck at the airport or abroad because your flight has been cancelled, you have a number of rights:

- Your airline should tell you what's going on. Ask at a check-in desk, but also look at its website, app and Twitter and Facebook for updates. Check the email you used when booking too, in case you've been sent an update.

- You may be entitled to food, drink, accommodation and communication costs. Regardless of what's caused the hold-up, your airline must look after you if you're waiting for an alternative flight because your original one was cancelled. They need to provide:

- A reasonable amount of food and drink (often provided in the form of vouchers).

- A means for you to communicate (often by refunding the cost of your calls).

- Accommodation, if you are re-routed the next day (usually in a nearby hotel).

- Transport to and from the accommodation (or your home, if you are able to return there).

If your airline can't immediately cover these costs or provide a voucher, you can buy your own and claim back the cost, but make sure to keep receipts – and remember that only reasonable expenses are covered. Check if your airline's website has any guidance.

You may also be entitled to compensation on top

If your flight was cancelled within 14 days of departure, and it's the airline's fault for the cancellation, you may also be due compensation on top of the above.

You could be entitled to up to £505 depending on how long you’ve been delayed when getting an alternative flight, and how far your journey is. It’s worth noting that this only applies to flights that departed from a UK/EU airport, regardless of the airline, or where a UK/EU airline landed at a UK/EU airport. Under these rules, EU airports also include those in Iceland, Liechtenstein, Norway and Switzerland.**